Download PDF

Authors

Onwumere Victor Onyekwere, PhD1; First Bank of Nigeria, Plc

Chukwu Luke Chukwuka , PhD2 ; Department of Accountancy,

Imo State University, Owerri

ABSTRACT

The study focused on the effects of deposit rates on banks’ financial performance. Three deposit money banks listed on the Nigeria stock exchange between 2008 and 2021 were selected for this study. The deposit rate was measured using CBN deposit rates while banks’ performance was measured with profit after tax, return on assets and return on equity. Dependency tests and normality tests were carried out to ascertain the appropriateness of the data in fitting into the study model. Three hypotheses were formulated and the models were estimated using Panel Least Square Regressing technique. Results show that deposit rate has a negative and insignificant effect on banks’ financial performance. The study therefore recommends that the apex bank should come up with policies that would help to improve the saving culture of the people, without much increase in the deposit rate

Keywords: Deposit, Deposit rate, Interest Rate, Savings, Financial Performance.

INTRODUCTION

Deposit money banks have been widely acknowledged for their significant role in the economy particularly in funds mobilization for growth in both developed and developing countries of the world. One of the basic aspects of banks which enhance its performance is the deposit rate (Ajayi & Oke, 2022). According to Okechi (2021) increase or growth in the volume of deposit enhances the ability of banks to create credit by lending to prospective customers who have been found creditworthy in character. Increase in lending is expected to boost the level of investment that is investment in financial assets, real assets, production activities and businesses generally which would in the long-run engender economic growth. However, decline in the volume of deposit would have a reducing effect on the lending ability of banks and investment in an economy, thus significantly retarding economic growth. In an unstable foreign exchange rate situation, with high exchange rate in favour of foreign currencies, the role of domestic currency deposit cannot be over-emphasized, as exchange rate affects the foreign currency deposit element of bank deposits(Sutiman, 2022).

To correct this imbalance, the economy has to look inwards, and embark on the strategy of import substitution industrialization, thus reducing foreign currency transactions (Alawiye-Adams & Ayodeji, 2016). In Nigeria, since the advent of the former president, the Muhammadu Buhari-led regime in 2015, the economy witnessing serious hike in foreign exchange rates; and as such, attention has to be drawn in favour of domestic currency deposit and the key factors that determine its inflow, as this would help the monetary authorities and bank management make informed decisions on monetary matters, which, in the long-run, would engender economic growth(Baba and Ashogbon, 2019). As a result, when interest rates change (especially deposit rate), as is seen from the unstable interest rate regime in Nigeria, such fluctuations in interest rates have the potential to damage both the overall performance of banks and the economy of a nation as a whole. The discovery of inflationary pressures by the Central Bank of Nigeria led to the establishment of an interest rate policy, which was then implemented and used to regulate the circulation of money in the economy.

This policy was used to control the circulation of money in the economy. Deposit money banks in Nigeria were forced to restrict their borrowing after the Nigerian central bank made the decision to raise the interest rate that banks pay to borrow money. As a result, deposit money banks in Nigeria experienced a significant decline in both their overall operations and performance (Hassan, 2016). However, deposit money banks also increased their deposit rate in the business environment and to other borrowers. This resulted in fewer loans and advances and decreased the quantity of money in circulation throughout the economy. Individuals, businesses, and industries have been dissuaded from taking loans and advances as a direct result of the high interest rate, which has resulted in less money in circulation, a decrease in credit, and a fall in prices (Akinwale, 2018). In all, the extent of economic performance depends on deposit rate; hence this work focused on deposit rate and financial performance of deposit money banks in Nigeria (2008 – 2021).

Statement of the Problem

Deposit money banks are the most important savings, mobilization and financial resource allocation institutions. Consequently, these roles make them an important phenomenon in economic growth and development. One of the reasons depositors deposit their money in the bank is to ensure for its safe keeping and have financial control over their expenditure pattern. However, other benefits/incentives that arises from the deposits has made depositors to adjust their deposit pattern. While some keep their fund in a savings account that gives little interest rate, others have considered fixing their funds for a specified period of time so as to attract more interest earned on deposit. This interest earned by depositors otherwise called deposit rate has been interpreted to have different effects on the banks financial performance. While some authors such as (Ayo, 2017) argued that as an expenses, which is incurred by the bank, it will reduce the bank’s profitability, others countered this argument stating that it will attract more funds into the banks that can be used to financing loans which has a higher interest earning for the banks(Acho, 2021). Why these arguments continue to exists, the thrust of this study is to ascertain empirically the effects deposit rate has on financial performance of deposit money banks in Nigeria.

Objective of the Study

The major objective of the study is to examine deposit rate and financial performance of deposit money banks in Nigeria (2008 – 2021). Specifically, the study is designed to:

- Evaluate the effect of deposit rates on profit after tax of deposit money bank.

- Examine the effect of deposit rates on return on asset of deposit money bank.

- Ascertain the relationship between deposit rates and return on equity of deposit money bank.

Research Questions

Based on the objective of the study, the following research questions were formulated to guide the study:

- What are the effects of deposit rates on profit after tax of deposit money bankin Nigeria?

- To what extent does deposit rates effects return on asset of deposit money bankin Nigeria?

- What isthe relationship between deposit rates and return on equity of deposit money bankin Nigeria?

Research Hypotheses

In view of the above research questions and objectives, the following hypotheses were formulated to guide the study:

Ho1: Deposit rates has no significant effect on profit after tax of deposit money bank in Nigeria.

Ho2: There is no significant effect of deposit rates on return on asset of deposit money bankin Nigeria.

Ho3: There is no significant relationship between deposit rates and return on equity of deposit money bank in Nigeria.

REVIEW OF RELATED LITERATURE

This chapter is organized under conceptual review, theoretical and empirical.

Conceptual Review

Independent Variable Dependent Variables

Fig. 1: Operational Conceptual Framework.

Source: The Researcher, 2023.

Interest Rate

According to Keynes cited inOrbunde, Lambe and Anyanwu (2022), interest is the reward for not hoarding but for parting with liquidity for a specific period of time. Keynes’ definition of interest rate focuses more on the lending rate. Adebiyi (2001) defines interest rate as the return or yield on equity or opportunity cost of deferring current consumption into the future. Some examples of interest rate include the saving rate, lending rate, and the discount rate. Jhingan (2003) defines interest as the price which equates the supply of ‘credit’ or savings plus the net increase in the amount of money in the period, to the demand for credit or investment plus net ‘hoarding’ in the period. This definition implies that an interest rate is the price of credit which like other price is determined by the forces of demand and supply; in this case, the demand and supply of loanable funds. In general terms, interest rates can be defined as the amount due (in form of compensation) per period, as a proportion of the amount lent, deposited, or borrowed otherwise known as the principal sum.

The total interest on an amount lent or borrowed depends on the principal sum, the interest rate, the compounding frequency, and the length of time over which it is lent, deposited, or borrowed. According to Kalsoon and Khurshid (2016), interest is more or less the fee that is paid for using the funds of another person. It is paid when we borrow and received when we lend. When the borrower pays back the loan he also pays interest with the principal payment. He argued that if there is no concept of interest no one would be interested to lend. In this study, interest rate in the banking sector is viewed from one perspective: “the amount due as compensation to deposits mobilized”. It is important at this point to understanding the relationship between interest rates as defined in this study, and net interest margins.

Typically bank “lend long and borrow short”. That is, the average maturity of the loans in a bank’s portfolio tends to exceed the average maturity of its deposits and other debt. Hence, when interest rates fall, banks’ funding costs usually fall more quickly than their interest income, and net interest margins rise (Wheelock, 2016). In other words, Net Interest Margin (NIM) is a measurement comparing the net interest income a financial firm generates from credit products like loans and mortgages, with the outgoing interest it pays holders of savings accounts and certificates of deposit. NIM is a profitability indicator that approximates the likelihood of a bank or investment firm thriving over the long haul. It is an important indicator that helps potential investors determine whether or not to invest in a given financial services firm by providing visibility into the profitability of their interest income versus their interest expenses (Bloomental, 2022).

Deposit Rates

Deposit is one of the components of bank liabilities, and it serves three purposes (Gallemore, Mayberry & Wilde, 2017). First, deposit serves as an instrument of money creation. Second, deposit growth boosts the volume of savings in an economy. Third, deposit is used as one of the two variables in the calculation of the level of money supply in an economy. These roles are so important that, without deposit, the ability of banks to create money would not be sustained. Also, savings is necessary to boost the level of investment that is needed for the growth process. Furthermore, in an economy, demand de posits with banks function as one of the indicators of Narrow Money (NM). Accordingly, Pradhan and Paneru (2014) stated that bank deposit represents the most significant component of the money supply used by the public, and a change in money growth is highly correlated with change in the price of goods and services in the economy. As a result, changes in the inflow of deposits exert greater effects on the ability o f banks to create money and, at the same time, investment. Essentially, key deposit determinants vary from country to country: While Rachmawati and Syamsulhakim (2004) identified profit sharing rate and number of branches as key determinants of deposit in Indonesia, Finger and Hesse (2009) identified interest rate differential, prices at macro level and riskiness of individual banks, liquidity buffers, loan exposure, and interest margins at micro level as determinants of deposit in Lebanon.

While Eriomo (2015) identified bank investment, bank branches, interest rate and general price level as key determinants of bank deposit in Nigeria, Boadi, Li and Lartey (2015) identified savings interest rate as the most imperative factor that determines deposit in Ghana. Essentially, Ayodeji and Ajala (2019) classified these determinants into two; these are macroeconomic determinants (e.g. interest rates, inflation rates, exchange rates, and gross domestic product) and bank-specific determinants (e.g. credit to private sector, number of branches, bank size, credit rating and customer relations). Unfortunately, in Nigeria, there is dearth of literature on the effects of deposit determinants on domestic currency deposits. For, available studies on the subject matter are those of Eriomo (2015), who investigated the macroeconomic determinants of commercial bank deposits in Nigeria; Olutoye (2015), who assessed deposit volume and SMEs financing in Nigeria; and Ayodeji and Ajala (2019), who considered the effects of deposit volume and its determinants on economic growth in Nigeria. This situation creates a notable lacuna in the area of domestic currency deposit and its macroeconomic and bank-specific determinants. For Ali-Momoh&Fajuyagbe (2022), deposit domestic currency deposits are the amounts placed in bank accounts, which are basically denominated in the currencies of the domestic economy (for example, bank deposits denominated in Naira and Kobo in Nigeria), and are so placed for keep and/or interest earning.

Essentially, domestic currency deposit is the total bank deposit less foreign currency deposit. It comprises demand deposit, savings deposit and time deposit. It could be simply referred to as bank deposit (assuming foreign currency deposit is zero or non-existent); and as such, Olutoye (2015) simply stated that, bank deposits are made to deposit accounts at a banking institution, such as current accounts, savings accounts, and money market accounts (i.e. fixed deposit accounts). The account holder has the right to withdraw deposited funds as set forth in the terms and conditions of the account. Essentially, domestic currency deposits can be subdivided into three; these are savings deposit, current account deposit (demand deposit), and fixed deposit (Onipede&Ayodeji, 2005; Ayodeji&Ajala, 2019). In the light of the foregoing, the first type of domestic currency deposit is demand deposit, which is a deposit made into a current account. This type of deposit does not earn interest, but it is used to generate revenue for the bank in the form of commission on turnover. However, holders of this type of account need not give the bank a notification before withdrawal, and there is no limit to the number of times withdrawals can be made. This accounts for why it is called demand deposit: for, the bank must meet the withdrawal request of the customer when made (i.e. on demand).

However, it is the practice of some banks to give interest on current account s, from which no withdrawal was made in a month, thus enjoying the benefits enjoyable under a savings account system. The second type of domestic currency deposit is savings deposit, which is deposit made into savings accounts. Intrinsically, savings account is majorly a retail account for varieties of customers; and this type of account can be accessed at all times, and it has a floating interest attached to it (Bikker&Gerristen, 2018). The floating interest here means that the savings accounts earn interest monthly, provided the intermediation process of the bank is not disrupted by the customer’s number of withdrawals. For, when a customer withdraws more than three times in a month, the customer, usually, forfeits the accruable interest. This type of deposit is used by banks to carry out their short-term lending functions. Before, now, the account holder used a passbook when he or she operated the account. The passbook was meant to be presented at the counter before any lodgment or withdrawal could be effected. The account holder could only check his/her balance, and withdraw money from the account by appearing personally in the banking hall (Onipede&Ayodeji, 2005). However, in today’s banking system, the adoption of electronic banking has made it easier for customers to access their accounts by checking their balances, effect withdrawals and transfers without appearing physically in the banking hall.

The third type of domestic currency deposit is called time deposit, that is, fixed deposit. This type of deposit has a fixed maturity, which prevents the customers from early withdrawal (Bikker&Gerristen, 2018). It enhances the bank’s ability to invest in medium to long term financial assets, which generate more income in the form of profit to the bank. Holders of fixed deposit accounts earn interest on their deposits, which are greater than those of savings accounts, and the interest rate is determined by market forces based on the threshold of treasury bills rate, being a money market account. In addition, withdrawal of this deposit requires notification for termination (Onipede&Ayodeji, 2005). Worthy of note is the fact that deposit is essential to the continued existence and t he performance of the intermediation function of banks. Just as human beings cannot do without oxygen, banks cannot perform their financial intermediation functions of savings mobilization and lending without deposit. More importantly, deposit serves as an indicator of management effectiveness when banks record high growth of deposit at the lowest cost.

Bank Financial Performance

Bank financial performance tools and ratios include operating income, earnings before interest and taxes, Total Asset value. Financial performance analysis is carried out to ascertain the profitability position and performance of a firm. It can be conducted by management, owners, creditors, investors. According to Orbunde, Lambe and Anyanwu (2022),financial performance is the measure of how well a firm can use its assets from its primary business to generate revenues. To them, it can be measured by variables which involve productivity, profitability, growth or even customers’ satisfaction. The measures of financial performance includes dividend per share, Return on Assets (ROA), Return on Equity (ROE), profit after tax, Return on Investment (ROI), residual income (RI), earning per share (EPS), and dividend yield, growth in sales etc (Stanford, 2019). In this study, financial performance of banks could be measured through dividend per share, return on asset, bank profit after tax and return on equity. They were discussed thus:

- Return on asset: According to Porter and Kramer (2012), Return on Assets (ROA) is an indicator of how profitable a company is relative to its total assets. ROA gives a manager, investor, or analyst an idea as to how efficient a company’s management is at using its assets to generate earnings. Some investors add interest expense back into net income when performing this calculation because they’d like to use operating returns before cost of borrowing. Sometimes, the ROA is referred as “return on investment” (Porter and Kramer, 2012). In basic terms, ROA tells us what earnings were generated from invested capital (assets). ROA for public companies like bank can vary substantially and will be highly dependent on the industry. This is why when using ROA as a comparative measure, it is best to compare it against a company’s previous ROA numbers or against a similar company’s ROA. Remember that a company’s total assets are the sum of its total liabilities and shareholder’s equity. Both of these types of financing are used to fund the operations of the company. Since a company’s assets are either funded by debt or equity, some analysts and investors disregard the cost of acquiring the asset by adding back interest expense in the formula for ROA.

- Bank profit after tax:After deducting the taxation amount, the business derives its net profit or profit after tax (PAT). Profit after tax or a gain after tax is essentially the amount of money that remains with the taxpayer after all the necessary deductions have been made. It is like a barometer that tells you how much profit a business has really earned. Profit After Tax is the total amount that a business earns after all tax deductions have taken place. It is used as a barometer to determine how much a business really earns and how much it can utilize for its day to day activities (Norman & Health, 2004). Profit after tax is also seen as a measure of a company’s profitability after all its expenses have been deducted and can be fully utilized by the company to conduct its business. Shareholders are also paid dividends from this amount. The profit after tax is often a better assessment of what a business is really earning and hence can use in its operations than its total revenues. After tax profit margin is a financial performance ratio, calculated by dividing net profit after taxes by revenue. A company’s after-tax profit margin is important because it tells investors the percentage of money a company actually earns per dollar of revenue (Mughal &Akram, 2012).

Profit after tax is the total net amount earned by a business after all tax expenses have been deducted or settled (Ezeugwu&Akubo, 2014). Profit after-tax is the earnings of a business after all income taxes have been deducted. This amount is the final, residual amount of profit generated by an organization. The profit after-tax figure is considered the best measure of the ability of an entity to generate a return, since it incorporates both operating income and income from other sources, such as interest income. To them, in analyzing profit after tax, the following issues are noted:

- Profit After Tax is an important measure of the company, since it shows the actual amount that a company is making in that operating year. It shows the cost and the cash earnings of the company, which then determines the operational efficiency and performance.

- Often analysts pit companies’ profit after tax against other companies in the same market segment to compare the health of businesses. This figure is also used in other ratios and complex equations such as profit-after-tax margin, which gives a more objective and detailed look of the company. It is significant in showing the competency of a business in being able to turn its revenue into profits.

- Profit After Tax is often an effective figure used to calculate ratios which measure the profitability and efficacy of the company

- Profit After Tax margin uses PAT to show how any change in the value will manipulate the stock prices when the company is publicly listed.

- If the company is listed, Profit After Tax is calculated on a per share basis too and it appears on the income statement of the company.

- If the PAT value is high, it shows high efficacy and vice versa.

- PAT is directly proportional to the dividends paid to equity shareholders; more profit after tax, better dividends are paid.

- When the profit after tax is negative, it is considered as a loss and therefore it is not taxable. It makes the company unsustainable during a loss period.

- Return on equity: A potential investor assesses the company’s future by looking at the extent of the growth of the company’s profitability. And the indicator that is often used is Return on Equity (ROE), which illustrates the extent to which the company’s ability to generate profit that can be obtained by shareholders (Kamar, 2017). The high of ROE reflects that the company managed to generate a profit from its own capital. The increase of the value of ROE will increase the value of selling the company, which would certainly impact on stock price. In corporate finance, the return on equity (ROE) is a measure of the profitability of a business in relation to the book value of shareholder equity, also known as net assets or assets minus liabilities (Wikipedia, 2021). ROA is a measure of how well a company uses investments to generate earnings grown. In this direction, return on equity (ROE) is the amount of net income returned as a percentage of shareholders equity. Return on equity measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested (Mayende, 2013). Net income is for the full fiscal year (before dividends paid to common stock holders but after dividends to preferred stock). Shareholder’s equity does not include preferred shares.

Impact of Interest Rate on Customer Savings Behavior

The dynamics between interest rate and customer savings behavior has not been overly researched (Fasanya & Onakoya, 2020). While the topic has generated a lot of discussions, no conclusive agreement has been reached as to the nature of how interest rates is likely to affect customer savings behavior particularly in the Nigerian context, furthermore even if many studies have investigated the role of interest rate on savings within the growth and financial business cycle context few have tried to address customers savings concerns as a matter of primary interest using a non parametric estimation technique as we do in this study (Ogunmuyiwa, 2019). A host of factors are likely to affect customer saving behavior in banks, some include the fixed saving interest rates which is likely to affect customers incentive to save, country specific wage rates which will depict the average allowance available after the individual budget demands, aggregate average annual bank losses which is likely to affect customer perception of how well banks are doing, institutional and regulatory strength which depicts the level of oversight function and internal control effectiveness, average bank lending, and country specific monetary policy as exerted by the country’s apex financial agency such as the Central Bank (Sulaiman&Azeez, 2021).

Fixed savings account interest rates can also have strong consequences on overall average bank deposit and in most cases it is also affected by bank specific lending interest rates since it is customer deposits that are lent to private sector business with the expectations of returns on borrowed capital, making nominal interest rates to have a back-effect on fixed savings interest rates. Nominal interest rates therefore is likely to have an indirect causal effect on customer savings through fixed savings account interest rates which will probably be true since interest on savings are likely to be paid from returns on borrowed capital obtained from nominal interest on borrowed capital (Ajayi&Oke, 2022). Low interest rates has been known to drive output production in many developed economies, as it creates enabling environment for private business expansion through the provision of easy access to capital for further production purposes. In December 2013, the United States all share index continued to soar amidst the Fed report to maintain interest rates at an all time low following the withdrawal of the stimulus finally signaling an end to the US financial crises. While nominal interest rate depicts the riskiness of the business environment it can also be used as a tool by a country’s federal regulating agency in time of crisis for financial stabilization and quantitative easing of the economy.

Theoretical Review

The theories used arethe market power theory, financial liberalization theory, and modern portfolio theory.

The Market Power Theory

This theory was developed by Tregenna in 2009. The theory is mostly applied in banking and it states that the performance of bank is influenced by the market structure of the industry. According to Tregenna (2009), there are two distinct approaches within the theory namely the Structure-Conduct-Performance (SCP) and the Relative Market Power hypothesis (RMP). According to the RMP hypothesis, the profitability of commercial banks is influenced by market share. The assumption underlying this hypothesis is that, only large banks with differentiated products can influence prices and increase profits. They are able to exercise market power and earn non-competitive profits. Smaller banks don’t have the ability to influence prices and increase profits (Tregenna, 2009).

The SCP approach on the other hand, states that the level of concentration in the banking market gives rise to potential market power by banks, which may raise their profitability. Banks in more concentrated markets are most likely to make abnormal profits by their ability to lower deposits rates and to charge higher loan rates as a results of collusive (explicit or tacit) or monopolistic reasons, than firms operating in less concentrated markets, irrespective of their efficiency (Tregenna , 2009). The discussion of the market power theory shows that bank financial performance is a function of external market factors. The theory is relevant to the study as it explains how dividend per share, profit after tax, return of equity and return on assert of the deposit money banks can be linked to market factors which form the macro economic factors.

Financial Liberalization Theory

Financial liberalization theory owes its origin to the seminal works of Mackinnon (1973) and Shaw (1973). Proponents of this theory lean on the supply-lending relationship between growth and development. The theory believes that when real interest rates are high, it increases the level of financial deepening and the level of savings resulting in a more efficient allocation of financial resources among productive sectors. Following Classical economics, interest rate is seen as providing the returns for choice. When interest rates are kept artificially low Shaw (1973) submits that it will result to shallow financing. The central argument of the theory is that financial repression and indiscriminate distortion of financial prices including interest rate and exchange rate will lead to both a decrease in depth of the financial sector and a loss of efficiency with which savings are intermediated.

According to Mackinnon (1973) the desire to hold money relates in a positive manner with the rate of returns on capital. The shortcomings of this hypothesis is that it was developed on the premise that all investments are self-financing which is an over simplification of modern financial environment where money is by nature socially embedded. The holding of money even in the simple rural setting discussed by McKinnon is not simply driven by investment needs, the productivity of capital and real return on holding money but mostly by social obligations and other constraints.

Modern Portfolio Theory

This theory was developed by Markowitz in 1952. The modern portfolio theory (MPT) is a theory of finance that attempts to maximize expected portfolio returns for a given amount of portfolio risk, or equivalently minimize risk for a given level of return by carefully choosing the proportions of various assets. MPT models a portfolio as weighted combination of assets, so that the return of a portfolio is the weighted combination of the assets return. The process of selecting a portfolio may be divided into two stages. The first stage starts with observation and experience and ends with beliefs about the future performances of available securities.

The second stage starts with the relevant beliefs about future performances and ends with the choice of portfolio. One type of rule concerning choice of portfolio is that the investor does (or should) maximize the discounted (or capitalized) value of future returns. Since the future is not known with certainty, it must be “expected” or “anticipated” returns which are discounted. Through combining different assets whose returns are not perfectly positively correlated, MPT seeks to reduce the total variance of the portfolio return. MPT also assumes that investors are rational and the markets are efficient.

Empirical Review

Orbunde, Lambe and Anyanwu (2022) examined the impact of interest rate on the financial performance of listed manufacturing firms in Nigeria from 2009 to 2018. The dependent variable of the study was financial performance measured by Return on Assets (ROA) and Return on Equity (ROE), while the independent variable was Interest Rate (ITR). Secondary data on financial performance was obtained from the annual reports and accounts of 28 sampled manufacturing companies for the period 2009 – 2018 while data for interest rate was obtained from the Central Bank of Nigeria (CBN). Correlation research design was adopted and cross-sectional/time series data was extracted from the reports of the firms, while and panel multiple regression was used to analyze the data in order to establish relationship between the variables using Eviews-10.The findings showed that interest rates had a significant impact on ROA but no significant impact on ROE of listed manufacturing firms in Nigeria.

Baba and Ashogbon (2019) focused on interest rate and financial performance of commercial banks in Nigeria. The analysis of the effect of interest rate on financial performance of commercial banks in Nigeria is important. The study used panel data regression model to establish the relationship between the predictor and the independent variables. Panel data refers to the pooling of cross-section data over several time periods. The data employed in this study was panel in nature since for each of the 23 banks (or cross-sections) data on selected variables influencing return on equity (inflation rate) was tabulated over the period 2006 – 2015. The findings indicated that real interest rate is negatively and significantly associated with the performance of commercial banks in Nigeria.

Egbunike and Okerekeoti (2018) investigated the effect of interest rate, inflation rate, exchange rate and the Gross Domestic Product (GDP) growth rate, while the firm characteristics were size, leverage and liquidity. The dependent variable financial performance was measured as Return on Assets (ROA). The study used the ex-post facto research design and the population comprised all quoted manufacturing firms on the Nigerian Stock Exchange. The sample was restricted to companies in the consumer goods sector, selected using non-probability sampling method. The study used multiple linear regressions as the method of validating the hypotheses. The study found no significant effect for interest rate and exchange rate, but a significant effect for inflation rate and GDP growth rate on ROA. Second, the firm characteristics showed that firm size, leverage and liquidity were significant.

Hasan, Islam and Wahid (2018) examined the impact of some selected macroeconomic variables on the performance of 32 non-life insurance companies of Bangladesh over the period of 7 years (2009–2015) giving rise to 224 panel observations. Two performance measures, like Return on Asset (ROA) and Return on Equity (ROE) were used as dependent variables. The explanatory variables were inflation rate, GDP growth rate, interest rate, and exchange rate. The research employed panel data regression methodology. The regression results suggested that inflation rate, GDP growth rate and exchange rate, except interest rate, had no statistically significant influence on the performance of non-life insurance companies.

Mordi, Adebiyi and Omotosho (2019) in their study on “modelling interest rates pass-through in Nigeria: an error correction approach with asymmetric adjustments and structural breaks” documented some robust evidence on interest rate pass-through in Nigeria. The study made use of co-integrating vector error correction method as data analysis technique. Their work confirms, among others, that a long-run relationship exists between interest rates and banks performance. The study further shows that the transmission of changes in MPR to the retail market is not complete and that bank retail rates (except the savings rate) adjust symmetrically to changes in the policy rate. They further find that it takes about fourteen months for shocks to the policy rate to be passed fully to the prime lending rate, while the full impact on the 6-month deposit rate takes place in about eleven months.

Altavilla, Boucinha and Peydró (2018) in their study on “monetary policy and bank profitability in a low interest rate environment”, argue that many studies in this area could be biased because they don’t fully account for the common effect of GDP on bank profits and interest rates. They include macroeconomic forecasts as additional controls using a multiple linear regression technique and find no robust association between interest rate changes and euro area banks’ profitability in the short run. They found that profitability is lower during prolonged periods of low interest, but the estimated effect is small – about 2½ basis points for each additional year in a low-interest environment.

Borio and Gambacorta (2017) in their study on “the influence of monetary policy on banks’ profitability” with multiple regression analysis method, find a large effect of interest rates on the profitability of large advanced economy banks. They estimate that a 100 basis point fall in interest rates is associated with a 25 basis point fall in banks’ ROA after one year, with this effect increasing up to 40 basis points when interest rates are very low.

Bikker and Vervliet (2017) researched on “bank profitability and risk-taking under low interest rates”. The study employed a dynamic and static modelling approaches and regression estimation techniques as method of data analysis. They find that the low interest rate environment indeed impairs bank performance and compresses net interest margins. They also find that lower interest rates have a negligible effect on US banks’ profitability, mainly because higher fees and lower loss provisions offset downward pressure on Net Interest Margins.

Kalsoon and Khurshid (2016) reviewed the impact of interest rate spread on profitability. The study concludes that there exists a positive and significant relationship between interest rates and the profitability of banks. Overall, the available evidence indicates that lower interest rates typically have a negligible to modest negative effect on bank profitability in the short run. This is at least partly because of the positive effect that lower interest rates have on economic growth and banks’ asset quality, which offsets the negative effects of lower interest rates on NIMs. However, there is evidence that bank profitability falls further when interest rates are at low levels and remain low for a prolonged period. Smaller banks’ profitability is also more sensitive to lower interest rates, both in the short and longer run.

Udude (2015) examines the impact of interest rates on savings in Nigeria’s economy between 1981 and 2013. The study also investigated the joint influence of savings and income on total savings in the economy. Ex-post facto research method was employed and the hypothesis was tested using the VAR test. Findings from the analysis showed that interest rate combined with GDP has a positive and significant effect on savings.

Alessandri and Nelson (2015) in their study on “Simple Banking: Profitability and the Yield curve” examined how interest rates affects bank profitability. Their study made used of linear regression technique and the study found that increases in market interest rates compress interest margins thereby leading to a reduction in profitability.

Busch and Memmel (2015) researched on bank net-interest margin and level of interest rates. The study made use of linear regression techniques as data analysis method. The study found that net interest income benefits over the medium to the long-term horizon if the interest rate level increases. An increase of a 100 basis point fall in the level of interest rates is associated with a 7 basis point contraction in the Net Interest Margins of German banks.

Kamunge (2012) in his study on “the effect of interest rate spread on the level of non-performing loans of commercial banks in Kenya”, used multiple regression models to examine the effect of interest rate on non-performing loans. Non-performing loans served as the dependent variable while interest rate spread, debt collection cost, and credit appraisal cost served as independent variables. Regression results led to the conclusion that there is a positive relationship between the level of nonperforming loans and interest rate spread. Results also indicate that interest rate spread and debt collection cost were statistically significant in explaining level of nonperforming loans.

Okech (2021) undertook a study on the effect of lending rates on the performance of commercial banks in Kenya. It used regression through secondary data. The study considered management efficiency and operating cost efficiency, in regard to lending interest rate. The study found that a weak positive relationship between lending rates and performance of commercial banks. Since interest rates accounted for only 14.4% of the revenue in commercial banks, the study recommended income source diversification for better performance.

Kipngetich (2021) examined the effect on interest rates on the performance of commercial banks in Kenya. It used regression through secondary data. The study used published incomes statement of commercial banks between 2006 and 2010 to model the relationship between interest rates and financial performance. The study concluded that in the short term, interest rates did not have a significant effect on profitability of commercial banks.

Suliman (2022) carried out a study on the effect of interest rate on the economic growth of Nigeria. Annual time series data covering the period from 1970-2020 was used. The empirical analysis was carried out using econometric techniques of Ordinary least squares (OLS), Augmented Dickey-Fuller unit root test, Johansen Co-integration test and error correction method. The co-integration test shows long-run relationship amongst the variables and findings from the error correction model revealed that interest rate has contributed positively to the growth of the Nigerian economy.

Ajayi and Oke (2022) investigated the effect of bank lending on economic growth and development of Nigeria. They used national income as an endogenous variable and debt service payment, external reserve and interest rate as exogenous variables. They found that banks’ lending had a positive effect on the nation’s income and per capital income.

Sulaiman and Azeez (2021) examined the effect of bank deposit on the economic growth of Nigeria. Gathering annual time series data from 1970-2018. Employing econometric techniques of Ordinary Least Square (OLS), Augmented Dickey Fuller (ADF) unit root test, Johansen Co-integration test and Error Correction Model. The result of ADF shows that all the variables were stationary at first difference with the exception of inflation rate. Johansen co-integration depicts that all the exogenous variables except external debt has a positive long run relationship with GDP. The result of Error correction model shows that bank deposit has positive but insignificance relationship with GDP.

RESEARCH METHODS

Research Design

In this study, the researcher employed quasi-experimental research design for the study. A quasi-experimental study examines how an independent variable, present prior to the study, affects a dependent variable. This will be used because the study focused on secondary data.

Secondary data sources were utilized for the study. The data were sourced from the three banks’ annual reports between 2008 and 2021 (14 periods of 42 observations) and central bank of Nigeria statistical bulletin. The nature of the data is panel data. Banks performance was proxied with Profit after tax, return on asset and return on equity while interest rate was proxied with deposit rates.

Model Specification

The model used for this study was specified to show the functional relationship between interest rate and performance thus:

The model can be specified econometrically as:

The model can be transformed to reflect its log form as follows:

β0 – slope of the model; PAT – Profit After Tax

β1– coefficients to be estimated; ROA – Return on Assets

ԑ – stochastic error; ROE –Return on Equity

i – Individual bank t – Time period.

– Deposit Rates Asset – Control Variable

Panel Least Square Regression method of analysis was adopted for the model estimation. Some diagnostic tests such as normality test and dependency test were carried out to check the adequacy of the data and its appropriateness in fitting into the study model.

Data Analysis

Dependency Test

| Table 3: Residual Cross-Section Dependence Test | |||

| Null hypothesis: No cross-section dependence (correlation) in residuals | |||

| Total panel observations: 42 | |||

| Cross-section effects were removed during estimation | |||

| Test | Statistic | d.f. | Prob. |

| Breusch-Pagan LM | 1.7541 | 3 | 0.7183 |

| Pesaran CD | -0.7152 | 0.6132 | |

| Source: Researcher’s Computation using E-views 7 | |||

Source: Researcher’s Computation using E-views 9

One of the diagnostic tests carried out in this work is the dependency test, so as to confirm that the disturbances in panel data models are cross-sectionally independent. The study employed Breuch-Pagan (1980) LM and Pesaran (2004) CD dependence test to ascertain the presence of cross-sectional dependence in the residuals. Both Breusch-Pagan LM and Pesaran CD tests accept the null hypothesis at 0.05. Analysis shows that there is no cross-sectional dependence in the residual, hence the panel data is suitable for regression (P-Value 0.71 and 0.61 respectively).

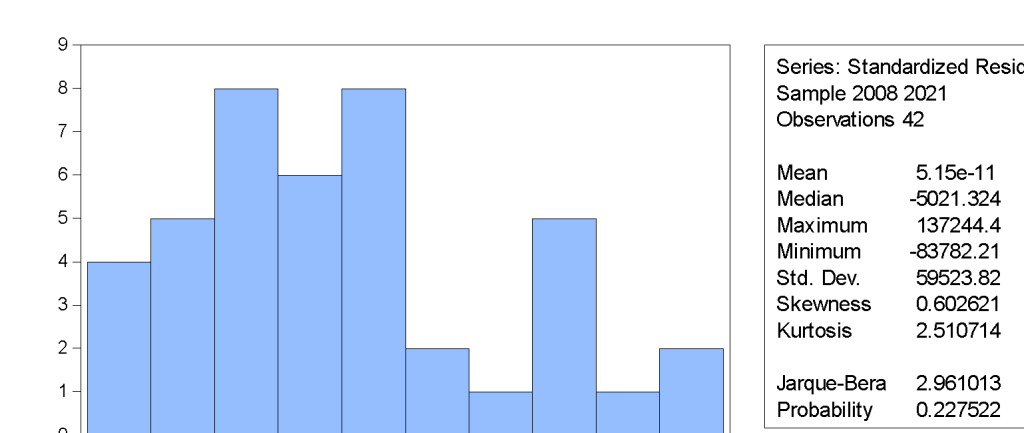

Figure 1: Test of Normality

Source: Researcher’s Computation using E-views 9

To ensure that the data set had a normal distribution, a normality test was carried out. The test shows the aggregated averages of the mean, median, and standard deviation which are measures of spread and variation, skewness which looks at the symmetry, and Kurtosis which looks at the centrality of the peak. The overall Jarque-Bera statistics of 2.51 with a p-value of 0.23 accepts the null hypothesis that the data is normally distributed.

Panel Least Square Regression Result

The regression results as given in equation 7, 8, and 9 are presented below.

Table 4: Panel Least Square Regression Result for Equation 7

| Dependent Variable: LOGPAT | ||||

| Method: Panel Least Squares | ||||

| Total panel (balanced) observations: 42 | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| LOGDEPR | -1.015721 | 0.886523 | -1.145735 | 0.2589 |

| LOGASSETS | 0.639527 | 0.212292 | 3.012490 | 0.0045 |

| C | 1.925405 | 2.112130 | 0.911594 | 0.3676 |

| R-squared | 0.310455 | Mean dependent var | 4.866289 | |

| Adjusted R-squared | 0.275094 | S.D. dependent var | 0.355083 | |

| F-statistic | 8.779511 | Durbin-Watson stat | 0.596943 | |

| Prob(F-statistic) | 0.000711 | |||

Source: Researchers’ Computation

The coefficient of LOGDEPR shows that deposit rate is negatively related to banks profit after tax (LogPAT) but the relationship is insignificant. Its coefficient of -1.02 shows that a unit increase in deposit rate decreases profit after tax by 0.32 units and this coefficient is insignificant as p value is 26%.

Table 5: Panel Least Square Regression Result for Equation 8

| Dependent Variable: LOGROA | ||||

| Method: Panel Least Squares | ||||

| Total panel (balanced) observations: 42 | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| LOGDEPR | -1.425710 | 0.746505 | -1.365746 | 0.3589 |

| LOGASSETS | -0.360471 | 0.212287 | -1.698032 | 0.0975 |

| C | 3.925378 | 2.112087 | 1.858531 | 0.0707 |

| R-squared | 0.372548 | Mean dependent var | 0.349509 | |

| Adjusted R-squared | 0.024640 | S.D. dependent var | 0.306111 | |

| F-statistic | 1.517875 | Durbin-Watson stat | 0.596915 | |

| Prob(F-statistic) | 0.231843 | |||

From the analysis above, the coefficient of LOGDEPR shows that deposit rate is negatively related to banks performance measured with return on assets (LogROA). However, the relationship is insignificant. Its coefficient of -1.42 shows that a unit increase in interest rate decreases return on assets by 1.42 units and this coefficient is insignificant as p value is greater than 10 per cent (35%).

Table 6: Panel Least Square Regression Result for Equation 9

| Dependent Variable: LOGROE | ||||

| Method: Panel Least Squares | ||||

| Total panel (balanced) observations: 42 | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| LOGDEPR | -0.843665 | 0.802453 | -1.051357 | 0.2996 |

| LOGASSETS | -0.113047 | 0.192160 | -0.588294 | 0.5597 |

| C | 2.932636 | 1.911834 | 1.533938 | 0.1331 |

| R-squared | 0.027825 | Mean dependent var | 1.176971 | |

| Adjusted R-squared | -0.022030 | S.D. dependent var | 0.270687 | |

| F-statistic | 0.558122 | Durbin-Watson stat | 0.666945 | |

| Prob(F-statistic) | 0.576786 | |||

From the analysis in table 6 above, the coefficient of LOGDEPR shows that deposit rate is negatively and insignificantly related to banks performance measured with return on equity (LogROE). Its coefficient of -0.84 shows that a unit increase in interest rate decreases return on equity by 0.84 units and this coefficient is insignificant as p value is 29%.

From the analysis so far, it evident that deposit rate has an insignificant negative effect on banks performance. All the three performance models employed in this study has the same outcome of insignificant relationship between interest rates and banks performance indices. These findings are in agreement with the study of Altavilla, Boucinha and Peydró (2018) that found find no robust association between interest rate changes and banks’ profitability in the short run.It also correlates with the findings of Baba and Ashogbon (2019) who indicated that real interest rate is negatively and significantly associated with the performance of commercial banks in Nigeria.

Summary of Findings

This study has tried to ascertain the effects of deposit rate on performance indices of deposit money banks listed on Nigeria stock exchange. The study proxied deposit rate with deposit rate issued to banks from the apex bank. While performance was measured with three indices: Profit after tax, return on assets and return on equity. Finding from the study shows that:

- Deposit rate has no significant effect on profit after tax in the Nigerian banks.

- Deposit rate has no significant effect on return on asset in the Nigerian banks.

- Deposit rate has no significant effect on return on equity in the Nigerian banks.

Conclusion

Deposit/lending rate and its effects in the banking system has been argued over time by concerned stakeholders. While most of these studies focused on lending rates, much attention has not been given to deposit rates which is an interest expense from the banks’ perspective. While the lending rate remains significant on the profit of banks, its significance is greatly affected by the rate at which the funds were obtained. The study examined how deposit rate affects banks’ financial performance. The study reviewed two important theories related to interest rates such as the Keynesian theory of interest rate and the financial liberalization thesis. After a lot of empirical analysis, the study concludes that the deposit rate has a positive and insignificant relationship with banks’ financial performance.

Recommendations

Based on the findings of this study, it was recommended that the apex bank should come up with policies that would help to improve the saving culture of the people, such as an increase in the deposit rate which would attract the surplus sector to deposit their money in banks thereby increasing the supply of loanable funds. This will no doubt make many funds available for the deficit sector thereby leading to productive use of idle funds and affecting economic development positively.

REFERENCES

Ayo, N. (2017). Impact of interest rate and deposit on the growth of Nigeria economy.Global Economy and Finance Journal, 4(1), 4-32.

Acho, G.(2021). Problems of deposit rate in the Nigeria banks. The work did not consider the issue of bank performance. International Journal of Arts and Commerce, (2), 111-115.

Adebiyi, M.A. (2021). Can high real interest rate promote economic growth without fuelling inflation in Nigeria? Journal of Economic and Social Studies, 4, 86-100.

Ajayi, K. &Oke, P. (2022). The effect of bank lending on economic growth and development of Nigeria. Current Research Journal of Economic Theory, 2(2), 82-86.

Akinwale, S.O. (2018). Bank lending rate and economic growth: Evidence from Nigeria. International Journal of Academic Research in Economics and Management Sciences, 7(3), 111-122.

Alawiye-Adams, A.A. &Ayodeji, E.A. (2016). Rethinking Nigerian state for economic development through import substitution industrialization. International Journal of Banking, Finance, Management and Development Studies, 2(1), 1-16.

Alessandri, P. & Nelson, B.D. (2015). ‘Simple banking: Profitability and the yield curve’. Journal of Money Credit and Banking, 47(1), 143–175.

Ali-Momoh, B.O. &Fajuyagbe, B.S. (2022). Interest rate and financial performance of listed deposit money banks in Nigeria. Journal of Accounting and Management, 12(2), 77-93.

Altavilla, C., Boucinha, M. &Peydró, J. (2018). Monetary policy and bank profitability in a low interest rate environment. EconomicPolicy, 33, 531-586.

Ayodeji, E.A. &Ajala, R.B. (2019). Deposit volume, its determinants and economic growth in Nigeria (2000-2018): Advancing bank-intermediation theorem. International Journal of Banking, Finance, Management and Development Studies, 5(1), 23-42.

Baba, S. &Ashogbon, S.O. (2019). Interest rate and financial performance of commercial banks in Nigeria. Global Scientific Journal, 7(2), 375-383.

Bikker, J.A. &Gerristen, D.F. (2018). Determinants of interest rates on time deposits and savings accounts: Macro factors, bank risk, and account features. International Review of Finance, 18(2), 169-216.

Bikker, J.A. &Vervliet, T.M. (2017). Bank profitability and risk-taking under low interest rates. International Journal of Finance & Economics, 23(4), 1-16.

Bloomenthal, A. (2022). Net interest margin. Investopedia.

Boadi, E.F., Li, Y. &Lartey, V.C. (2015). Determinants of bank deposits in Ghana: Does interest rate liberalization matter. Modern Economy, 6, 990-1000.

Borio, C. &Gambacorta, L. (2017). ‘The influence of monetary policy on bank profitability’. International Finance, 20, 48–63.

Busch, R. &Memmel, C. (2015). ‘Banks’ net interest margin and the level of interest rates‘. Deutsche Bundesbank Discussion Papers No 16/2015.

Egbunike, C. &Okerekeoti, C. (2018). Macroeconomic factors, firm characteristics and financial performance: A study of selected quoted manufacturing firms in Nigeria. Asian Journal of Accounting Research, 3(2), 142-168.

Eke, F.A., Eke, I.C. &Inyang, O.G. (2015). Interest rate and commercial banks’ lending operations in Nigeria: a structural break analysis using chow test. Global Journal of Social Sciences, 14, 9-22.

Eriemo, N. O. (2015). Macroeconomic determinants of bank deposits in Nigeria. Journal ofEconomics and Sustainable Development, 5(10), 49-57.

Ezeugwu, C.I. &Akubo, D. (2014). Analysis of the effect of high corporate tax rate on the Profitability of corporate organizations in Nigeria. A study of some selected corporate Organizations. Mediterranean Journal of Social Sciences, 5(20), 310-321.

Fasanya, S. &Onakoya, A. (2020). The impact of interest rate and foreign aid on economic growth in Nigeria during the period of 1970-2017. Banks and Bank Systems, 13(4), 103-118.

Finger, H. &Hesse, H. (2019). Determinants of commercial bank deposits in a regional financial center. IMF Working Paper, No.09/195.

Gallemore, J., Mayberry, M. & Wilde, J. (2017). Corporate taxation and bank outcomes: Evidence from U.S. State taxes. University of Chicago, Florida and Lowa Graduate School of Business.

Hasan, M.B., Islam, S.N. & Wahid, A.N.M. (2018). The effect of macroeconomic variables on the performance of non-life insurance companies in Bangladesh. Indian Economic Review, 53, 369–383.

Hassan, O.M. (2016). Effect of interest rate on commercial banks deposits in Nigeria. Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and Social Sciences, 1-17.

Jhingan, M.L. (2013). Macroeconomic theory, 10th ed. New Delhi: Vrinda Publications.

Kalsoon, A. &Khurshid, M.K. (2016). A review of impact of interest rate spread on profitability. Journal of Poverty, Investment and Development, 25, 29-32.

Kamar, K. (2017). Analysis of the effect of Return on Equity (ROE) and Debt to Equity Ratio (DER) on stock price on cement industry listed in Indonesia Stock Exchange (IDX) in the year of 2011-2015. IOSR Journal of Business and Management, 19(5), 66-76.

Kamunge, H.T. (2012). The effect of interest rate spread on the level of non-performing loans of commercial banks in Kenya.International Journal of Business & Management Review, 2(1), 1-5.

Kipngetich, K.M. (2021). The relationship between interest rates and financial performance of commercial banks in Kenya. Unpublished Masters Thesis, University of Nairobi.

Mayende, S. (2013). The effects of tax incentives on firms’ performance: evidence from Uganda. Journal of Politics and Law, 6(4), 95-107.

McKinnon, R. (1973).Money and capital in economic development. The Brooking Institute: Washington DC.

Mordi, C.N.O., Adebiyi, M.A. &Omotosho, B.S. (2019). Modeling interest rates pass-through in Nigeria: An error correction approach with asymmetric adjustments and structural breaks. Contemporary Issues in the Nigerian Economy: A Book of Readings, Central Bank of Nigeria.

Mughal, M.M. &Akram, M. (2012). Reasons of tax avoidance and tax evasion: Reflections from Pakistan. Journal of Economics and Bahavioural Studies, 4(4), 217-222.

Ng’etich, O. &Wanjau, I. (2011). The impact of interest rate spread on the level of Non-Performing Assets in commercial banks in Kenya. Journal of the American Statistical Association, 74, 427-431.

Ngure, I.M. (2014). The effect of interest rates on financial performance of commercial banks in Kenya. Unpublished Masters Thesis, University of Nairobi.

Norman, Y.I. & Health, W. (2014). “What can the stakeholders theory learn from Enron?” Ethics and Economics, 2(2), 1-12.

Ogunmuyiwa, F. (2019). Whether interest rate promotes economic growth in Nigeria using time-series data from 1970-2007. Journal of Economics and International Finance, 2(12), 261-271.

Okech, F.O. (2021). The effect of lending interest rates on financial performance of commercial banks in Kenya. Unpublished Masters Thesis, University of Nairobi.

Olutoye, E.A. (2015). Effect of deposit volume on SME financing: Evidence from Nigerian banking sector. International Journal of Banking, Finance, Management and Development Studies, 1(2), 39-50.

Onipede, D. &Ayodeji, E.A. (2005). Economics for schools and colleges. Ibadan: Kins Publishers Limited.

Orbunde, B., Lambe, I. &Anyanwu, N. (2022). The impact of interest rate on the financial performance of listed manufacturing firms in Nigeria from 2009 to 2018. Bingham University Journal of Accounting and Business (BUJAB), 86-97.

Osamwonyi, I.O. & Michael, C.I. (2014). The impact of macroeconomic variables on the profitability of listed commercial banks in Nigeria. European Journal of Accounting Auditing and Finance Research, 2(10), 85-95.

Owoputi, J.A., Kayode, O.F. &Adeyefa, F.A. (2014). Bank specific, industry specific and macroeconomic determinants of bank profitability in Nigeria. European Scientific Journal, 10(25), 408-423.

Porter, P.C. & Kramer, T. (2012). Industrial relatives. London: Pearson Education Publisher.

Pradhan, R. &Paneru, D. (2014). Macroeconomic determinants of bank deposit of Nepalese commercial banks. http://dx.doi.org/10.2139/ssrn.3044098.

Rachmawati, E. &Syamsulhakim, E. (2014). Factors affecting Mudaraba deposits in Indonesia. Working Paper in Economics and Development Studies.

Sanusi, G. (2010). The magnitude and speed of the interest rate pass-through for Nigeria. Econometrics, 55, 251-276.

Shaw, E.S. (1973) Financial deepening in economic development. Oxford University Press, New York.

Stanford, M. (2019). Cash flow, earnings ratio and stock return in emerging global region. Global Economy and Finance Journal, 4(1), 4-32.

Sulaiman. J. &Azeez, M. (2021). The effect of bank deposit on the economic growth of Nigeria. Nigerian Financial Review, 9(3), 36 – 37.

Suliman, D. (2022). The effect of interest rate on the economic growth of Nigeria. Nigerian Economic and Financial Review, 1(1), 1-23.

Tregenna, F. (2009). The fat years: the structure and profitability of the US banking sector in the pre-crisis period. Cambridge Journal of Economics, Volume 33, Issue 4, July 2009, Pages 609–632, https://doi.org/10.1093/cje/bep025

Udude, T. (2015). The impact of interest rates on savings in Nigeria’s economy between 1981 and 2013. Journal of Finance, 60(4), 2043-2082.

Wheelock, D.C. (2016). Are banks more profitable when interest rates are high or low? Federal Reserve Bank of St. Louis.

Wikipedia, The Free Encyclopaedia (2021). Return on asset. www.wikipedia. org.

Zulfiqar, Z. &Ud Din, N. (2015). Inflation, Interest rate and firms’ performance: The evidences from textile industry of Pakistan. International Journal of Arts and Commerce, (2), 111-115.